PART 3 of 3

AFTER THE SS California steamed past the Statue of Liberty, the aging vessel berthed at Ellis Island. As Fazio Paolini and the passengers disembarked, they joined the daily throng of 5,000 or so fellow emigrants who had made the same arduous oceanic voyage and were now on their way through the same hallowed facilities. For first- and second-class passengers, there was little wait time. But even for steerage passengers, the process was efficient. If all went well, 98% of the applicants would be successfully admitted to their new homeland within hours. Contrary to common folklore, there were scant “lost in translation” moments, in which immigration officials arbitrarily spelled the new arrivals’ names in some Anglicized variation (changing “Paolini” to “Pauline,” for instance). Interpreters were available for all major European languages.

The next stop was an exchange station to convert currency. The passengers then purchased tickets for the ferry ride to the mainland, with a box lunch provided (courtesy of their new country) to enjoy on one last boat ride.1

burned downed a mere 3 weeks after he had passed through the facility. The iconic

stone structure seen here was completed in 1900.

It closed down operations in 1954 and opened as a tourist destination in 1976.

Imagine the sights and sounds of New York City in 1897. The five boroughs (still separate municipalities at the time) were already congested to the tune of 3.3 million people and 200,000 horses. By all appearances of film footage from the era, the “New York minute” was already a thing. The city was rapidly rising in its status as a world financial center, trading capital, shipping hub, and entertainment center.

For the middle and upper class, this was the Gilded Age, a sardonic term coined appropriately by Mark Twain, which referred to the era of excessive wealth. The New York affluent resided in Victorian mansions made of marble and granite, and the burgeoning middle classes occupied the iconic brownstones. There was electricity and steam heat, and trolley cars for transportation. Bicycles were all the rage, ranging in price from $10 to $100.2

Life was comfortable — and even entertaining — for the higher members of society.

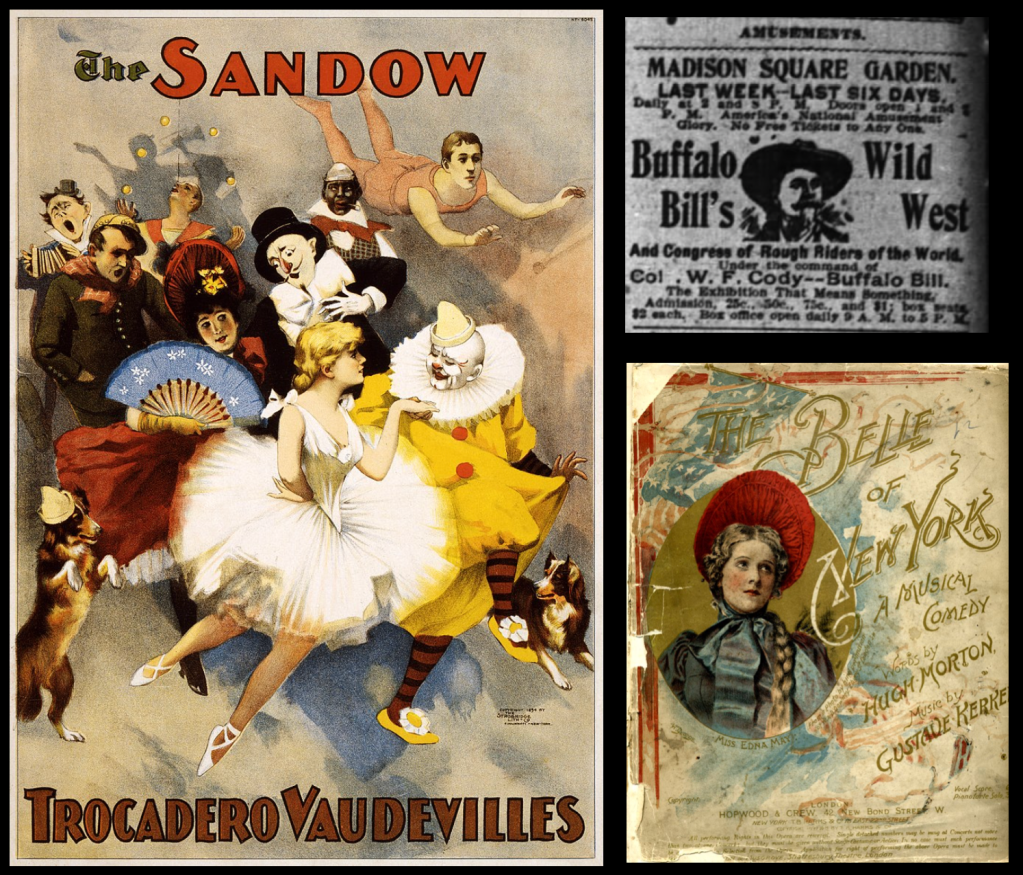

One could catch a performance of The Belle of New York on — where else? — Broadway, or perhaps hear Italian baritone Mario Antonio at the Metropolitan Opera House. For those who appreciated more prosaic forms of entertainment, there was Vaudeville, where acts included juggling, trapeze artistry, comedy, bawdy humor, and popular song. One of the more renowned shows in town at Madison Square Garden was none other than William F. Cody and his Congress of Rough Riders of the World. Tickets for this spectacle started at 25 cents.

Little wonder, with all the frivolity the city could offer, the last decade of the 19th Century would earn another nickname: The Gay Nineties.

BUT FOR THE MAJORITY of people in this megalopolis — some 2.3 million souls — the glamour of the upper class was just an elusive dream. Life for the underprivileged was as dismal as the boat ride that brought them to these strange environs. This disenfranchised mass of humanity was housed in one of countless, flimsy tenement houses that contained little to no running water, no bathrooms, and very little heat. And these wooden structures were prone to conflagration.

Not surprisingly, living in such close quarters also meant the rapid spread of communicative diseases, such as yellow fever, cholera, diphtheria, tuberculosis, and others.

The factories in which the lower class labored for 10 to 12 hours a day, six days a week, were either stifling hot or bone-chilling cold and noisy. Ventilation was inadequate, compounded by dust and other airborne particles. The workers toiled at machines, performing mind-numbing tasks. Factory workers might even be locked in during their work shifts, potentially condemning them to death in the event of a fire, as was the notorious case of the Triangle Shirtwaist Factory fire.

For immigrants such as Fazio, the discrepancy between the haves and have-nots would have been of little importance. He was ready to start a new life and to do what was necessary to succeed. In his first full day in the new land, Signore Paolini and the other 4,999 or so newcomers just off Ellis Island that day would have squandered no time seeing a show or the sites. They needed first to find shelter and food, and then to earn a living.

Securing a place to sleep on the first night would have been the highest priority, yet it would not have been difficult. For 7 cents, one could find a sleeping bunk in a crowded room with a dozen or so other individuals. This would have been an improvement to the hull of the ship, but probably not by much.

Attaining gainful employment would have been the more difficult task. There were plenty of jobs to be had, but not for everybody. Discrimination was not only rampant, it was unapologetically blatant.

It is most likely that Fazio took whatever job he could find to get established.

If he did not work in the myriad sweatshops at first, there were other options for Italians, almost all of them very dangerous. Among them were digging tunnels, laying railroads, and construction, most notably skyscrapers and bridges, such as the Brooklyn Bridge.

“I came to America believing the streets were paved with gold. The streets were not gold. They weren’t even paved. And then I learned that it was my job to pave them.”

Italian immigrant saying

There were three other occupations, however, that were available to Italian immigrants, and for the rest of his life, Fazio would be identified by one or all of them. These included:

–Brickyard worker

–Fruit vendor

–Farmer

It is quite likely that he began by laboring in the brickyards.

The evidence to support this postulation is largely based on two factors:

- In order to become a fruit dealer or farmer, an immigrant would have had to have possessed considerable capital to finance the new enterprise. There is no evidence to support the theory that Fazio was a man of such financial means.

- The location Fazio chose to settle was in the middle of New York State, along the Hudson River. This makes it very, very likely that he was working in the brickyards there.

Approximately 70 miles north of New York City, on the Hudson River, towns such as Newburgh, Beacon, Haverstraw, and New Windsor were humming with activity. The riverbanks of the renowned waterway on which these towns were situated were being mined for the massive amounts of clay and sand that lined the shores. These materials were then manufactured on-site into the ubiquitous rectangular building blocks used to erect the skyscrapers and other structures of New York City.

The brickyard jobs paid relatively well and even included housing. Italian, Irish, Romanian, and Hungarian immigrants were recruited right off the boat. At the time Fazio landed in the U.S., there were some 135 such manufacturing sites in Ulster and Orange counties, cranking out hundreds of millions of bricks each year. Virtually all the bricks used in The Big Apple from that time period until the early 1930s were supplied from the Hudson River manufacturers.

As welcoming as the jobs in the brickyards might have been, they were not without peril.

Some clay mines descended 200 or more feet into the Hudson River bank. Sand and clay are not the most stable soils. Mine collapses were a very serious risk. The most notorious incident was in the town of Haverstraw in 1906, when mine shafts were bored directly under the town. A good portion of the enclave’s commercial buildings and homes collapsed into the void, causing a landslide and fires. Miners and residents alike died in that tragedy.

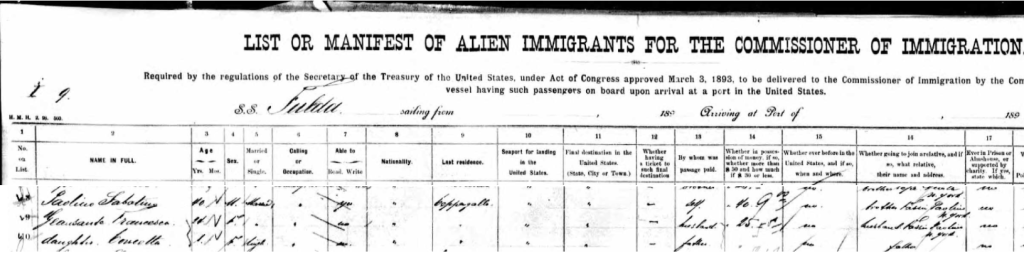

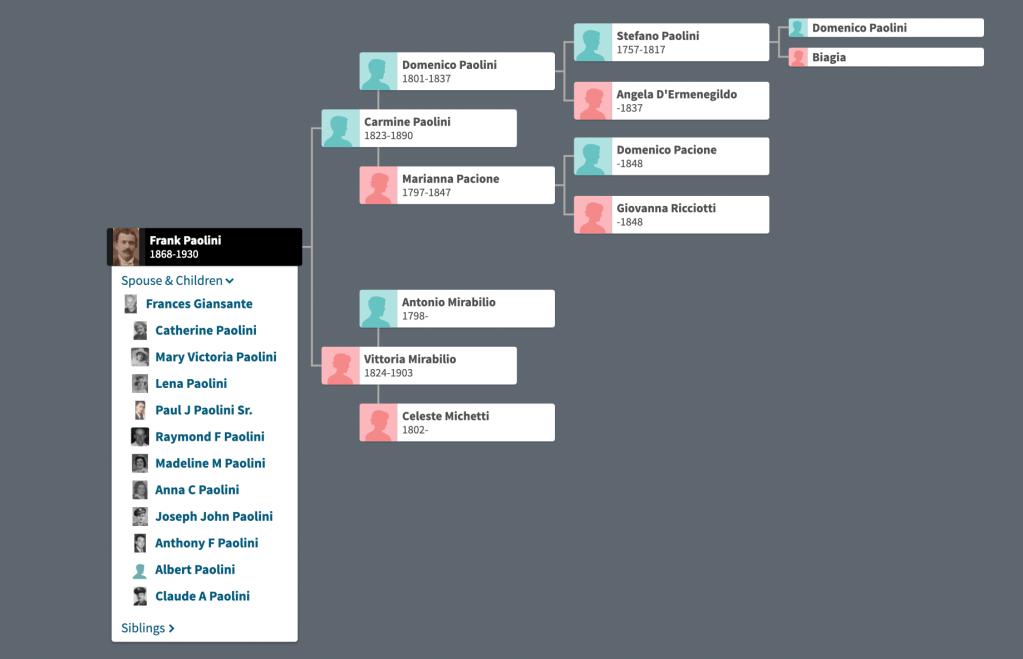

Whatever Fazio did to earn a living in 1897, this much is known: he earned enough in the first year to finance travel for his wife, Francesca, daughter Consetta, and brother Sabatino. Almost a year to the day from Fazio’s arrival in America, the three family members departed Naples, Italy on the SS Fulda, arriving on May 5, 1898, just in time for Fazio’s 30th birthday.

No doubt, that voyage was a difficult one, especially for Francesca and little Consetta. As noted in the previous chapter, traveling in steerage was dangerous at best for a woman. But, at least, Francesca had brother-in-law Sabatino to protect her against unwanted advances. And tiny Consetta clearly beat the odds of infant mortality aboard steamers, much to her mother’s gratefulness.3

In 1899, daughter Mary Victoria Paolini was born, and the birthplace is listed as Wappinger Falls. Located on the east side of the Hudson, this town was bustling with factories (20 of them). Wappinger Falls is adjacent to the town of Fishkill, where Brockway Brick Co. had mining and manufacturing operations. Whether Fazio was employed by Brockway at this time, we do not know for sure. But it does seem to be more than a coincidence.

But by 1900, the family was firmly established in Newburgh, New York. The census in that inaugural year of the new century lists Fazio and family at 225 Pine Street, Newburgh.9 And it is here that we see the Fazio listing his occupation as “fruit dealer.” My guess is that Fazio’s entrepreneurial endeavor was a side hustle more than his principal gig since he was an avid (and from accounts, successful) gardener. Sharing the “fruits” of his labor via a vending cart was a profitable hobby that he pursued his entire life.

The Verplanck years

AS WAS VERY TYPICAL of new immigrants, Fazio and his family moved quite a bit. There is no record of homeownership during their lifetimes. But without a doubt, the one place they called home that generated the fondest memories was a large, rather run-down mansion on Plum Point, overlooking the Hudson River in New Windsor, New York.

The structure was built by and once inhabited by one of the very first European families to settle in America: the Verplancks, a family of Dutch lineage that can trace its American ancestry to 1633, when New York was still known as New Amsterdam. (This was a mere 24 years after Henry Hudson sailed up the river that now bears his name.)

The Verplanck home was at this time owned by the Brockway Brick Company, which provided the domicile — as well as a few acres of land on which the house was situated — rent-free to Fazio, who was by this time a foreman of that company.

The exact dates during which Fazio Paolini and his family lived in this mansion are not clear. But a little guesswork, based on available records, suggests it was between 1911 and 1929. It was in this home that most of the children of Fazio and Francesca were born. My father, Claude, the youngest of the children, regaled his prodigy with stories of life on the farm. And I’m sure Claude’s siblings relayed similar stories to their children. Among the tales are these little anecdotes:

- The home had a unique design, with two identical entries. Each of these doorways was framed by a two-story-high portico, supported by six massive Doric columns. The younger boys — Joseph, Anthony, and Claude — would ride their bikes from one porch to the other, directly through the house, no doubt to the chagrin of their mother.

- Uncle Ray, the second oldest of the boys, was ever the prankster and troublemaker, teasing sister Madeline (Molly) to her wit’s end. One such escapade involved tying a string to the “water closet” and tripping the flushing mechanism from another room while Molly was seated.

- It was in this home that Raymond fell down the main stairway. His mother was in tears, believing him to have died in the descent. But he lived many years beyond that accident to tell the tale.

- Fazio had a massive garden that included prize-winning watermelons and grapes for fermenting his own wine.

- At some point, Fazio held the ceremonial title of deputy sheriff for Orange County. He took his role seriously, however, since on more than one occasion petty thieves or drunkards were held in the chicken coop until they could be remanded to official custody.4

- Fazio was also active in local society. According to newspaper articles, he helped to organize an annual town picnic at Plum Point. And, apparently, he remained active with his fruit cart, selling not only fresh produce but cigars, cigarettes, and ice cream at these town gatherings.

- A plow horse once suffered an intestinal obstruction. A veterinarian had the unenviable task of removing the blockage using nothing more than his hand and some lubricant. For the younger boys in the family, observing this “operation” was more entertaining than sneaking in the side door of the movie theater.

- Every farm must have a dog, of course. And the story of the family canine named Pat could have been the inspiration for the Disney tearjerker “Old Yeller.” Pat, apparently, became rabid, and eldest son Paul received the sad task of putting down the infected animal with his father’s gun. Before pulling the trigger, however, Paul bid his farewell to the beloved canine, with the now memorialized phrase: “Goodbye, Pat.” 5

- Fazio’s brother, Sabatino, was apparently quite the carpenter. He built, among other things, a beautiful dining table, crafted from cherry wood. He also made his own wooden vice, carving the screw by hand.

- There must have been some boisterous family dinners. One involved Fazio getting so angry that he pounded the corner of that cherry table with such force that the edge broke off.

From left to right, Anthony, Claude, and Joseph as boys at the time the family resided in the mansion on Plum Point. Could this be Pat the dog in the foreground?

It must have been one busy household. Sabatino (who changed his name to Samuel), was married and had children. If he and his family were not living with Fazio and his family at this time, he apparently was spending a considerable amount of time there.

And Consetta, who changed her name to Catherine (and was known to us as Aunt Kate), was married to Ercole Totonelly, and they had two children by 1915 as well. Records indicate they also lived in this home for some time.

Life during the Verplanck years had its share of grief, as well. Sabatino’s son, Anthony, died in his first year of life in 1914.

Albert Paolini, the twin of my father, Claude, died either in childbirth or as a result of the pandemic sweeping the country in 1918.

Daughter Mary died giving birth to her second child, John, in 1920.

There is no clear record of when the family moved out of the Verplanck residence. But it is highly likely that the Great Depression, which began to sweep across the country in late 1929, was the cause. By 1930, the homestead had been relocated to 245 Grand St. Apparently, Fazio maintained his job as foreman for the Brockway Brick Co. Records also show that daughter Lena was now married to Sebastian Scrivani and that they were living at that address as well.

The Fatal Fall

WHAT BEGAN AS A PROMISING spring day turned into a disaster of unimaginable proportions. And the Paolini family would never be the same from that moment on.

Sunday, March 9, 1930 was unseasonably warm and clear. Fazio, Francesca, and the family walked the 12 or so blocks from their home at 245 Grand St. to attend Mass at the Church of the Sacred Heart, in Newburgh.

It was the first Sunday of the Lent season. What sermon the Rev. Cyrus Falco6 delivered in the relatively new church that day, we do not know. But it is likely that Fazio, a devout Catholic, and an active church member, had not paid much attention to the pastor’s words on that morning. He had other things on his mind, especially regarding what was to transpire after the service.

The church, erected in 1912 to serve the needs of Italian Catholics in Newburgh, was not only close to home but was also located just one block from the Ford Motor Company’s dealership on Mill St. And immediately following Mass, Fazio and Francesca began to make the short walk to the auto showroom, while the children and grandchildren returned home. This was the day that Fazio and Francesca would purchase their first new automobile.7

This was a rather tenuous time to make such a large purchase. A new car, such as the Model A, was selling for somewhere between $500 and $800 (approximately $8,000 to $10,000 in today’s currency). That was a sizeable amount of cash to spend, especially since the stock market crash of the previous October ignited a panic that included runs on banks, in which panicked citizens were demanding to withdraw their savings. Banks could not keep up with the demand, and the institutions started failing.

But none of this would you know reading the front pages of the newspapers at the time. There was news, to be sure: William Howard Taft, the former president, and, at the time, Supreme Court Justice,8 had died that very day. Babe Ruth had just signed a record-breaking deal to renew his contract with the New York Yankees, and world-renowned aviator Charles Lindbergh had been thrown from a horse but survived intact, save the embarrassment.

And, if the advertisements in the newspapers were any indication, the economy was as robust as ever, with a high demand for new gadgets, such as an Atwater Kent Electro Dynamic Radio for $109 (or just $2 per week for one year after making a $5 down payment).

But there were hints of unrest. Unemployment was already on the rise to the extent that citizens took to the streets to protest. In New York City’s Union Square, apparently, 6,000 people showed up and were promptly labeled as Communists. Hence, the news was more about a “Red Scare” than the average citizen’s reaction to the historic economic collapse that was unfolding.

Yet, Fazio must have felt confident enough in his management role at Brockway Brick Company to not only contemplate but follow through with such a large purchase. Perhaps the acquisition of the automobile was to ensure he could continue to work on-site at the company since he would have had to commute the 5 or so miles from the family’s new residence to the Brockway factory. Whatever the incentive was for purchasing the new automobile that day, it all became moot within minutes of leaving the church.

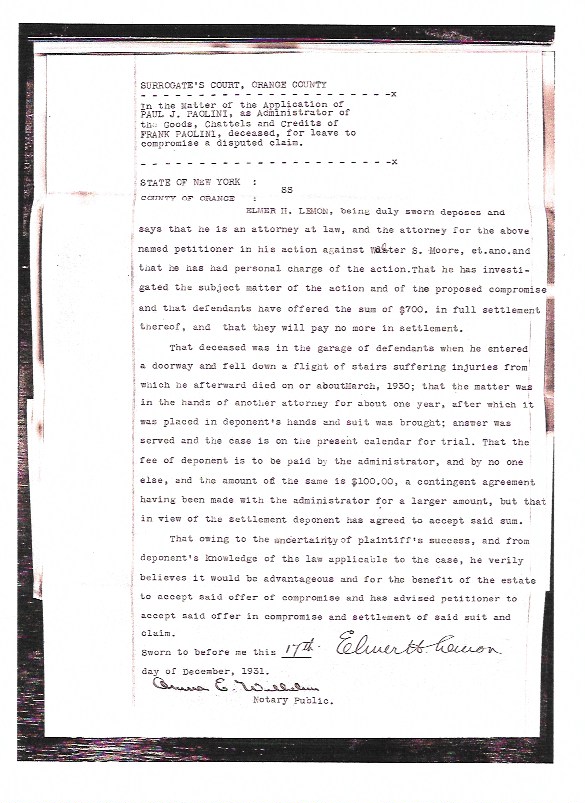

What really happened

For years, we knew the story. Grandpa Frank (Fazio) had died from a fall down a flight of stairs. As kids, we just assumed this fatal descent occurred on the farm and that his death came quickly. Whether our father knew the actual story or not, I’m not sure. He would have just turned 12 at the time. But his older siblings — Paul, Lena, Raymond, Molly at least — certainly knew.

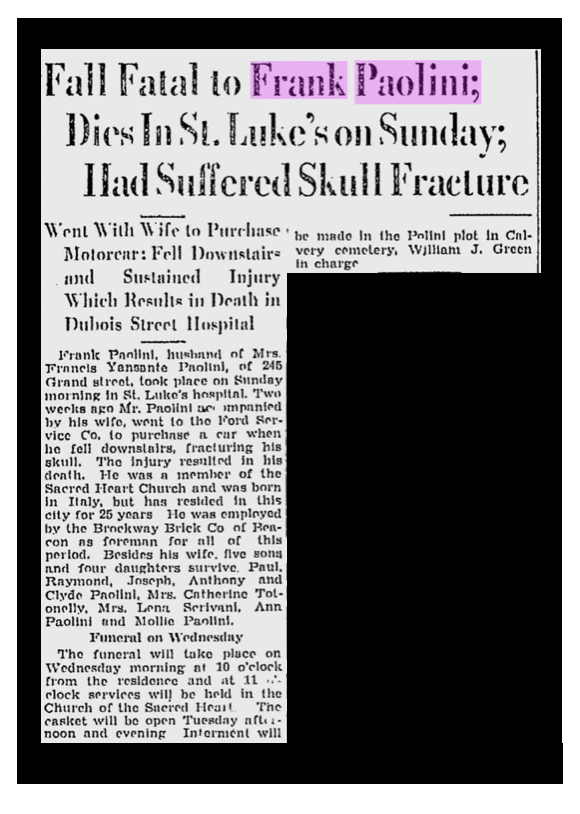

Exactly what happened on that fateful day is not entirely clear. But thanks to newspaper articles and legal documents, we know this much: Fazio and Francesca Paolini left the services at the Church of the Sacred Heart, walked around the corner, and entered the Ford dealership at 60-64 Mill St. with the intent of buying that new car. Once in the showroom, Fazio apparently went into the garage, presumably where the vehicles were serviced; quite likely he was planning to inspect the operation. But, unfortunately, he entered a doorway in the garage that, unbeknownst to him, led to a stairwell. Perhaps there was inadequate lighting. But somehow, Fazio fell down the flight of stairs, fracturing his skull.

From that moment, Fazio was unconscious and rushed to St. Luke’s hospital. He remained in the medical facility for two weeks, at which point he finally succumbed to his injuries. His funeral was held at the very same church that he had left that fateful Sunday morning, and the body was interred in Calvary Cemetery.

After getting over the shock of the accident, the family regrouped and decided to press charges against the Ford Motor Company. Paul, as the eldest male in the family, assumed command of the situation, spearheading the lawsuit. After 18 months, the litigation was settled out of court, and either the Ford dealership, the Ford Motor Company, or both, agreed to pay $700 without admitting guilt.

But even that pittance of remuneration must have been welcomed. By the time the suit was settled, the Great Depression was in full force. Every member of the family had to find a way to contribute. Even young Claude, who by this time was almost 14, dropped out of school to work.

The family persevered through that awful incident and the depression. Francesca would survive her husband for another 29 years. I only remember meeting her once, when she was very ill. She died on my fourth birthday: June 22, 1959. Her memorial service was held at the very same church as Fazio’s, and she rests next to him in the Paolini plot in Calvary Cemetery.

This is about all we know about Fazio and Francesca’s history and life. But, there are many things we can infer. To begin with, all of their children were decent, caring individuals, parents, aunts, and uncles, who made their contributions to family and society through honest and earnest work.10

The last reunion of their progeny — grandchildren and great-grandchildren — occurred in August 2014, at the very site of the Verplanck Mansion, which had been torn down many years prior. Well over 100 relatives from all corners of the United States attended.

Over the course of that weekend, we celebrated our common heritage and the uniqueness of our story. It is, of course, just one story, among the 12 million or so that passed through Ellis Island between 1892 and 1954.

Acknowledgements

For as long as I can remember, I have had a fascination with my family’s history. Fortunately, that enthusiasm has been shared by my siblings and many cousins. My goal in this narrative has been to put together the story for current and future generations.

I’d like to thank a number of people for their guidance, assistance, and support.

My late cousin Linda Paolini Gauthier was a big inspiration. She had visited the relatives in Cepagatti, Italy, and continued to research the family history beyond that trip. It was Linda and her sister, Joanne Paolini Diaz, that organized the reunion in 2014 and put together the framework for our family history that got me thinking about crafting this into a story. Cousin Carl Aiello also helped in this regard.

I was very fortunate to find a number of individuals who, despite having no incentive to help me, did just that. These include Glenn Marshall, the town historian in New Windsor, New York, and Pierangela Badia, who holds a similar title in Cepegatti, Italy.

Footnotes

- Contrary to popular belief, the process at Ellis Island was quite efficient. Passengers disembarked their ships with a passport and copy of information related to the ship registry and entered the Immigration building. There, they were interviewed (a list of 29 questions) to ensure they would qualify as upright citizens. The interview was conducted in their native tongue, to ensure accuracy. Interpreters of every major European language were available. The passengers were also required to undergo a physical exam to determine whether they were carrying any infectious diseases. Only 2% of all applicants were either detained for further questions or turned away altogether.

- In today’s dollars, those new bicycles would have cost between $337 to $3,378.

- As noted in the previous chapter, the passenger-ship mortality rate for children between the ages of 1 and 12 was 7.5%, and for infants, 19%.

- For years, I held in my possession a small leather notebook with a pen and pencil set, given to me by my father. On the cover, the words: “Frank Paolini, Sheriff” were embossed. New Windsor Town Historian Glenn Marshall assures me that the title was ceremonial in nature since there is no record of any Paolini being elected as a law enforcer in this time period.

- The story of Pat was told by Paul Paolini to his son Frank, who shared the anecdote in an essay memorializing his father.

- Reverand Falco is listed as the pastor of record at Newburgh’s Church of the Sacred Heart in 1930.

- I found it unusual that the Ford dealership would be open on a Sunday. (Even in the 1960s, when I was a child, very few stores were open on a Sunday.) But legal documents regarding the incident confirm this to be the date. Perhaps this was a grand opening for the dealership or some other special event.

- Taft is the only individual to hold the offices of the U.S. President and Chief Justice of the Supreme Court.

- The structure at 225 Pine Street in which Fazio and family first lived must have been demolished. A new home was built there in 1949, according to city records.

- There were tales of Uncle Ray Paolini smuggling booze from Canada during Prohibition. Legend has it that Ray drove a Packard wagon with a roof that had been modified into a flat tank to store and transport the contraband.

Fun facts

The five boroughs of New York — Manhattan, The Bronx, Brooklyn, Staten Island, and Queens were still separate cities in 1897. On Jan. 1, 1898, they incorporated as New York City. New York’s five boroughs were the home to myriad types of manufacturing at the turn of the 19th Century, including the making of drugs, chemicals, paint, furniture, and housewares such as china and glass. The processing of paper, raw cotton, and tobacco for shipping to other countries were also big industries.

At the time Fazio Paolini landed in New York, there were still 200,000 horses used for the transportation of people and goods. Each of these four-footed friends produced 24 pounds of manure and up to a half-gallon of urine per day. There was no adequate system for removing this animal waste.

Animal waste, garbage, and snow could pile up to six feet high in New York City. This is one of the reasons the famous Brownstones required a flight of stairs up to the first level, to rise above it all.

With the massive influx of 12 million new citizens, there was an abundant supply of labor, which kept wages excessively low. Regulations limiting worker hours and clamping down on the exploitation of child labor were still a few years away.

You must be logged in to post a comment.